Askeladden Shares Replay of Town Hall Showcasing Nominees' Specific and Relevant Experience

AstroNova's New Incentive Targets Riddled With Loopholes, Including Exclusions for MTEX and Goodwill Impairments

AstroNova Director Alexis Michas Claims Scheduling a Phone Call with Samir Patel is "Too Complicated"

1,000+ Aerospace Transactions Underscore Strategic-Alternatives Opportunity - Do Incumbents Prioritize Fiduciary Duty or Their Paycheck?

FORT WORTH, TX / ACCESS Newswire / June 16, 2025 / Dear AstroNova Shareholders,

Askeladden's recent town hall offered shareholders something the incumbent Board won't: direct, transparent engagement and a detailed plan for building a better AstroNova. A recorded replay is available here:

https://zoom.us/webinar/register/WN_P4nfq0iOSamSBEiaDZ0IZA#/registration

More information, including our Building a Better AstroNova presentation, can be found at askeladdencapital.com/astronova and in filings with the SEC.

We welcome all shareholders - large or small - to reach out to us directly. AstroNova's directors have a fiduciary duty to serve you. Please ask both sides your toughest questions, assess who offers a clear, evidence-based, and intellectually rigorous path to addressing AstroNova's failures and maximizing shareholder value, and vote accordingly.

While our town hall remained professional, polite, and focused on key issues, AstroNova's panicked communications have veered into ad hominem language and misleading characterizations.

We would prefer to focus solely on facts and solutions, but it's important to set the record straight. Below, we address five of the incumbent Board's more egregious claims, providing shareholders with the facts that AstroNova appears determined to obscure.

1. Shareholders Deserve Hands-on Board Engagement

2. AstroNova's New Incentive Plans: All Loopholes, No Accountability

3. Mr. Michas Claims Scheduling a Simple Phone Call is "Too Complicated"

4. Why Are AstroNova's Board Members Refusing To Evaluate Strategic Alternatives?

5. Incumbent AstroNova Directors Lack Print Industry Experience

1: Shareholders Deserve Hands-On Board Engagement

AstroNova's recent shareholder letter and presentation call Askeladden's proposed hands-on governance "appalling overreach." What's truly appalling isn't robust oversight: it's the incumbent Board's abdication of responsibility as shareholder value has imploded.

We interviewed over 20 former AstroNova employees and other industry veterans, many of whom have expressed harsh criticism about AstroNova's mismanagement - including the company's "dinosaur" marketing strategy, poor quality culture, and dysfunction directly attributable to the CEO and the Board.1 After years of shareholder value destruction, highly engaged governance is critical to righting the ship.

It's hardly unprecedented for an activist to propose or implement detailed operational changes based on extensive research. In 2014, activist fund Starboard Value famously published a nearly 300-page report on Darden Restaurants (the parent company of Olive Garden), analyzing operational details as specific as the number of breadsticks served per table and the lack of salt in the pasta water.2

After winning 12 Board seats with the backing of both ISS and Glass Lewis,3 Starboard implemented many of these proposals, while spearheading other successful initiatives such as discounted wine for patrons waiting to be seated, though they remained flexible (ultimately deciding to leave the pasta water unsalted). Starboard's highly engaged, research-backed approach delivered measurable results: 18 months later, Darden had delivered six straight quarters of positive same-store sales and a nearly 60% increase in shareholder value.4 To be clear: we are making no predictions or assurances of a similar result here.

Askeladden's nominees do not intend to manage day-to-day operations. Our role is to ensure the right strategy, the right leaders, and a culture of accountability. As the company's largest shareholder, we have the most to lose - or gain - from AstroNova's performance. As discussed in our public plan and during our town hall, we will prioritize a small number of high-impact initiatives to avoid overwhelming the organization's capacity for change. Several of these (such as modernizing the marketing strategy) have been advocated by AstroNova employees for years, but have fallen on deaf ears.

While the entrenched board repeatedly refers to our plan as "Samir's plan," this mischaracterization ignores the breadth of our nominees' experience. Our plan was jointly developed by our entire slate, meshing my extensive primary research with Mr. Oviatt's perspective as a public-company CEO and Board member, Mr. Kravetz's background in strategy consulting, extensive experience as a micro-cap investor, and public Board experience, Mr. Roberts' experience in integrating and growing a key business unit, and Mr. Sands' hands-on experience turning around dozens of businesses, including a Boeing supplier twice the size of AstroNova Aerospace.

The incumbent Board's characterization of our proposals as "overreach" or "disruptive" reflects Mr. Woods' fear of oversight that finally prioritizes shareholders and refuses to tolerate excuses. We indeed intend to disrupt incumbents' historical approach of rubber-stamping Mr. Woods' agenda despite breaking promise after promise. Mr. Woods:

Promised at the end of FY22 that ink issues were nearly resolved - they weren't. The issues dragged on for two more years, costing millions and causing brand damage.5

Promised in 20236 that inventory would come down - it did not. Q1 FY26 inventory days on hand now exceed FY23 year-end levels and remain ~50% above FY18 and FY19.7

Promised EBITDA growth in FY25 and FY268 - and delivered declines instead. FY26 EBITDA is now expected fall below FY24 levels.

Promised MTEX was a profitable, growing business9 - it was not. Instead, MTEX has lost money every quarter and recorded a $13.4 million goodwill impairment less than a year after its acquisition.10

Promised MTEX had built a "strong backlog"11and results would meet original expectations - instead, revenues remained at less than half of original expectations, and have declined sequentially since Q3 FY25.

Many of AstroNova's claims lack basic intellectual rigor. They claim the MTEX integration is "substantially complete"12 and needs no further review. Meanwhile, their Form 10-Q discloses that MTEX lost over $1 million in Q1 FY26. If AstroNova defines a $1 million quarterly loss as a complete and successful integration, we'd hate to see their definition of failure.

Similarly, AstroNova dismisses our proposed listening tour as too extreme - even though engaging directly with customers and employees is a well-established best practice for new leadership.13 Classifying a known best practice as "disruptive" epitomizes the Board's unwillingness to take even the most basic steps toward operational excellence. We recently spoke to a TrojanLabel customer who was happy to take our call - the real "disruption" he faced was the 400,000 misaligned and therefore unusable labels delivered by AstroNova, which threatened to shut down his production line and severely disrupt his business.14 Zeroing in on key customer and employee concerns is the first step to building a better AstroNova for all stakeholders.

2: AstroNova's New Incentive Plans: All Loopholes, No Accountability

AstroNova touts a new three-year incentive program as evidence of good governance and management alignment. Yet the company has missed every Short-Term Incentive Plan target since FY2020 - five of eight earned 0%.15 It defies logic to present yet another new incentive plan as the solution; moreover, long-suffering shareholders deserve improvements sooner than three years from now.

Worse yet, AstroNova's Compensation Committee has established a plan riddled with alarming "adjustments" - i.e., loopholes. These "adjustments" provide management and the Board a sweeping license to redefine success after the fact. Footnote 2 in the recent shareholder letter states their Adjusted EPS measurement will:

"exclude the impact of non-recurring items, as approved by the Committee, such as restructuring charges, impairment charges, and unbudgeted gains or losses outside the control of management"

Under this language, losses from another value-destroying deal like MTEX - which triggered a $13.4 million impairment less than a year after a $20+ million acquisition - would be swept under the rug. Similarly, "unbudgeted gains or losses outside the control of management" is an exclusion so thoroughly vague that it renders the exercise useless: any deviation from budget can be deemed "outside the control of management" and thus ignored.

The company's short-term plan for FY26 is no better. Page 4 of AstroNova's recently filed 8-K provides the following laundry list of "adjustments" to its operating cash flow:16

"adjusted to exclude MTEX-related acquisition expenses, inventory step-up costs and restructuring charges, each net of taxes, and such other items as may be approved by the Committee."

Once again, "such other items" is a broad and vague exclusion. It appears "Adjusted Operating Cash Flow" may bear little relation to actual cash flow, and instead be whatever figure the Committee deems convenient.

3: AstroNova Uninterested In Meaningful Engagement with Askeladden; Mr. Michas Claims Scheduling a Simple Phone Call is "Too Complicated"

AstroNova's recent shareholder letter made false and misleading claims about their engagement with Askeladden. They reference a text sent by Alexis Michas to Samir Patel on Tuesday, June 10; below is the full, time-stamped exchange.17 We invite shareholders to review these texts for themselves and decide who attempted to engage in good faith.

9:42 AM CT / 10:42 AM ET

Michas: "Samir this is Alexis Michas. [REDACTED] gave me your number. Do you have some time to talk to Darius [Nevin] and me today at noon New York time?"

11:53 AM CT / 12:53 PM ET:

Patel: "Hi Alexis, thanks for reaching out. I'm unavailable today and most of this week. Does Friday afternoon or Monday afternoon work for you and Darius? I will need to check schedules with Shawn [Kravetz] as well as he'll be joining the call from our side. Probably also easier to coordinate by email."

12:27 PM CT / 1:27 PM ET:

Michas: "Unfortunately I am on a plane to Europe Thursday night. Can you talk tomorrow or Thursday? I am only offering to talk to you at this point."

2:07 PM CT / 3:07 PM ET:

Patel: "Alexis - I understand your travel schedule but I had repeatedly requested the Board in March to collaboratively engage with Askeladden to address our concerns, with no response over the past several months. As mentioned, I am tied up most of this week and cannot rearrange my schedule on such short notice, so perhaps we can connect Friday afternoon, over the weekend, or sometime next week.

I suggested that Shawn join the call given that you were planning to have Darius join as well. I'm fine excluding Shawn; however, may I suggest that Mr. Baltay and Mr. Hitchcock [AstroNova and Askeladden's counsel, respectively] join instead? At this stage, I think it's in both of our best interests to avoid any verbal statements being misconstrued. We certainly remain open to a collaborative and amicable approach to addressing AstroNova's performance and governance challenges that could spare both sides further time and cost, and we look forward to a hopefully mutually productive exchange of perspectives with you and your colleagues in the near future."

4:15 PM CT / 5:15 PM ET:

Alexis Michas: "No worries. This all sounds too complicated. I just thought it would have been helpful to have a quick call to give you my perspective on all of this."

Note Mr. Michas' statement that he was calling simply to offer "my perspective," rather than expressing any interest in understanding our concerns as AstroNova's largest shareholder. The company's latest shareholder letter now suggests that Mr. Michas was, in fact, calling on behalf of the company.

This is not how serious engagement works. Formal matters of corporate governance during a proxy contest should not be handled via text message. After we informed the company of our intent to nominate directors, AstroNova made no contact with us for nearly three months, then Mr. Michas abruptly proposed a call on roughly an hour's notice. Beginning eighteen minutes later (at 11 AM ET), I had a two-hour call with the CEO of another Askeladden portfolio company, which had been planned for weeks, overlapped the proposed timeslot, and could not be rescheduled at a moment's notice for Mr. Michas's convenience.

With respect to Mr. Michas' specific points: Askeladden had numerous prior commitments over the next several days, including our ISS presentation, our previously-announced town hall, and another company's earnings report. I nonetheless responded to both of Mr. Michas's texts within several hours, providing him with my soonest availability and clearly communicating Askeladden's eagerness to constructively and amicably engage with AstroNova to resolve the ongoing proxy contest. To avoid any doubt on this topic, we will, shortly after publication of this letter, once again email AstroNova to reiterate our openness to a collaborative and amicable approach to improving AstroNova's performance and governance. Mr. Michas may be unavailable in Europe, but we never heard from Mr. Nevin, who was also supposed to be on Mr. Michas' proposed call and who presumably is not out of the country.

If Mr. Michas had reached out even a few days earlier, I could have cleared time to speak to him on Tuesday. Perhaps planning ahead is simply too much for AstroNova's directors - they doubled down on Memjet exposure by acquiring Astro Machine less than two years prior to acquiring MTEX to diversify away from Memjet.18

While claiming his travel schedule prevented conversation after Thursday - as if internet and cell service are unavailable in Europe - Mr. Michas made no attempt to connect us with any of AstroNova's five other directors for a call after Thursday, as we proposed. Instead, he lamented, "this all sounds too complicated." If scheduling a simple phone call is "too complicated" for Mr. Michas to handle, what does that imply for his capability to discharge his other, vastly more serious responsibilities as a director of AstroNova? This is not how serious boards operate.

AstroNova continues to accuse us of being a "distraction" - yet they are clearly making no effort to engage with us to arrive at a mutually agreeable solution, even though in March, we repeatedly requested them to take a collaborative, behind-the-scenes approach.

Our concerns about being misconstrued during a verbal conversation without the presence of additional witnesses appear well founded, since AstroNova subsequently chose to present this exchange in a very slanted way.

As for the referenced call with director Richard Warzala on March 14, we discussed this in detail in our proxy statement: the call was originally requested in February. We were originally informed that AstroNova would not communicate with shareholders until April, well after the nomination deadline, despite publicly promising a comprehensive update in March. Neither Mr. Warzala nor any other director responded to our emails after we communicated our intention to nominate directors, until Mr. Michas sent a text on June 10.

Shareholders should ask what really motivated AstroNova's quickly-abandoned effort to "engage" with us the week of ISS presentations and Askeladden's town hall. Their outreach - which they gave up on merely hours later as "too complicated" despite Askeladden expressing genuine interest in working towards an amicable solution - appears designed less to foster collaboration and more to check a procedural box so they could publicly claim they had reached out. Perhaps they even aimed to distract us from our own time-sensitive preparations for meetings with ISS and other shareholders.

Despite the company's misrepresentation of what actually occurred, we remain open to genuine engagement, as we clearly communicated to Mr. Michas last week, and will once again communicate directly to the company today.

4: Why Are AstroNova's Board Members Refusing To Evaluate Strategic Alternatives?

AstroNova disingenuously claims that our strategic alternatives proposal is based on a single comparable transaction. Instead, as we have communicated many times, our rationale begins with a simple fact: AstroNova operates two unrelated businesses, and its corporate overhead as a public company consumes a significant portion of segment-level profitability. In FY25, AstroNova generated over $20 million in segment-level operating income excluding the $13.4 million MTEX goodwill impairment, but this was substantially offset by $15.8 million in corporate expenses. We believe an acquirer could achieve substantial synergies at the segment level while also eliminating substantial corporate overhead - an acquirer would immediately obviate audit fees, listing costs, and of course Board and CEO compensation, which are generating negative ROI for shareholders given years of shareholder value destruction.

We have highlighted Servotronics several times due to its relevance: it has similar revenues to AstroNova Aerospace, was a public company with years of underperformance, and still attracted multiple bidders in May 2025 despite macroeconomic concerns raised by tariffs. Yet Servotronics is merely one data point: there is a long and well-documented history of aerospace businesses achieving attractive multiples in transactions, which AstroNova's Board should be aware of. A May 2025 report by Objective Investment Banking & Valuation cites 124 Aerospace & Defense transactions in Q1 2025 alone, with an average or median TEV/EBITDA multiple of 13.2x.19 This report cites over 1,000 transactions occurring between Q2 2022 and Q1 2025 with an average or median multiple ranging between 7x and 17.7x, although the median seems to be in the low double digits.

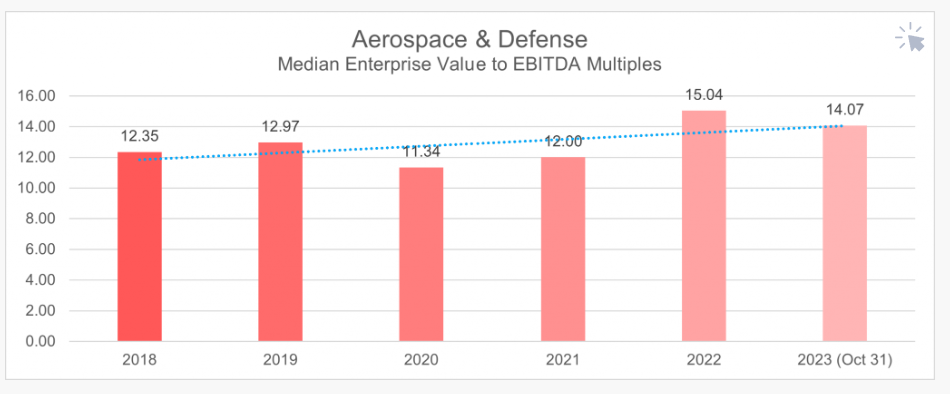

Similarly, another report from the Institute for Mergers, Acquisitons, and Alliances20 cites median Aerospace & Defense EV/EBITDA transaction multiples ranging from ~11.3x to ~15x from 2018 - 2023, although the lowest median multiples occurred during the COVID pandemic - if we exclude 2020 and 2021, the lowest median multiple was 12.3x.

Finally, earlier this year, publicly-traded aerospace components manufacturer Triumph Group announced a sale to Warburg Pincus and Berkshire Partners at approximately 16.6x EBITDA.21 Given the dominant market share, high aftermarket mix, and high margins of AstroNova Aerospace, we believe that it would achieve a competitive multiple at or above historical medians / averages if marketed.

According to AstroNova's Form 10-K for FY25, AstroNova Aerospace generated over $11 million in segment operating income in FY25, with segment EBITDA of nearly $12.5 million; furthermore, significant royalty payments to Honeywell will expire over the next few years due to contractual terms agreed upon at the time of acquisition, regardless of any actions management is taking.22

Thus, if sold at a valuation in line with historical medians, gross sale proceeds for AstroNova Aerospace would comfortably exceed AstroNova's entire current enterprise value, allowing AstroNova to repay all debt and distribute cash to shareholders roughly equivalent to the company's current market capitalization.

Shareholders would then retain debt-free ownership of the Product Identification business - a ~$100 million business with 80% recurring revenue and roughly $10 million of segment-level profits (with $4 million of upside potential if MTEX-related losses are eliminated). We believe it would be attractive to a strategic acquirer with the strong go-to-market capabilities that AstroNova lacks. While we decline to speculate on multiples, we believe shareholders can do their own math and come to their own conclusions: even conservative assumptions suggest a compelling outcome.

We find it telling that incumbents dismiss our clear, evidence-based analysis. With AstroNova's share price languishing around $9 - down roughly 50% since the Board approved the disastrous MTEX acquisition - shareholders should ask: is the Board's priority to maximize shareholder value, or entrench themselves and continue earning a paycheck?

The Board was willing to budget $1 million and spend months of effort entrenching themselves through this proxy contest - rather than even responding to our emails in March suggesting we negotiate, at zero monetary cost, to identify mutually agreeable directors and make governance improvements. Conversely, the Board doesn't even want to investigate whether shareholders could achieve substantial and immediate returns by selling one or both segments of the company.

As the company's largest shareholder, I have committed to foregoing compensation if elected as a director - my sole motivation is to maximize value for all shareholders.

While the remaining Askeladden nominees deserve compensation for their time and expertise, they too share my single-minded focus on maximizing shareholder value - even if the best path to doing so is a sale of the company that results in the conclusion of their Board service, and thus their paychecks.

5: Incumbent AstroNova Directors Lack Print Industry Experience

AstroNova's Board continues to criticize our nominees for lacking print-industry experience, yet glaringly fails to apply the same standard to itself. AstroNova's own biographies presented in their proxy statement do not cite meaningful operating experience in the print industry, prior to joining AstroNova, for any current director. Mr. Nevin, their most recent appointee, appears to have none - his last operating role was as the CFO of security company Protection One. Ms. Schlaeppi's only industry exposure was a legal role over a decade ago - not in an operating or commercial capacity. It seems the only print experience that other incumbents bring to the table is the trail of shareholder value destruction they've overseen at AstroNova - including the MTEX debacle.

Meanwhile, our slate has conducted deep due diligence - engaging with over 20 former employees and industry veterans to evaluate customer pain points, go-to-market failures, and technology risks. That's far more research than the Board appears to have done before committing over $20 million of shareholder capital to a money-losing business operating in a new market segment with a very different business culture and a lack of reliability and business process apparently widely known in the industry.

Through our research, we have developed relationships with several former key leaders at AstroNova as well as other industry peers; we intend to continue to leverage those relationships - including by potentially appointing one or more of these individuals as strategic advisors - to align AstroNova's operations with proven industry best practices.

If experience matters, shareholders should value those who learn rigorously - not those who repeatedly fail and call it expertise.

Conclusion

We could easily highlight many additional misrepresentations. For instance, slide 12 of AstroNova's presentation proclaims "another record year in FY26" - a claim based on revenue, not profits. FY26 EBITDA and EBITDA margin are expected to decline versus FY24, despite the company's deployment in FY25 of over $20 million of shareholder capital to acquire MTEX, and their announcement of $3 million of cost cuts. Touting success based on revenue growth - without analyzing measures such as free cash flow or return on invested capital - demonstrates a lack of commitment to shareholder value.

The Board continues to shift the goalposts rather than confront performance failures head-on. Incumbents make empty promises of future improvements, but their recent investor presentation contains not a single chart of the shareholder value destruction they have wrought, and glosses over their track record of broken promises. Instead of taking responsibility for their mistakes and attempting to collaborate with us to fix them, they malign us with personal attacks.

AstroNova's Board has had years to deliver value - and failed. We're asking for your support so shareholders can finally get the oversight they deserve. Our goal is to restore accountability, ensure an evidence-based strategy, and maximize shareholder value. This company's performance, governance, and capital allocation must change - and the current Board has proven either unwilling or unable to do it.

Thus, we urge all shareholders to vote FOR all Askeladden nominees using the GOLD proxy card.

If you wish to ask questions, share your perspective, or better understand our research, we would love to speak to you directly. We believe shareholder engagement should be transparent, thoughtful, and two-sided. Sadly, the incumbent Board does not appear to agree.

This is your company. This is your vote. And this is your chance to demand the change AstroNova so clearly needs.

Sincerely,

Samir Patel

Founder and Portfolio Manager - Askeladden Capital

samir@askeladdencapital.com

(682) 553-8302

Samir Patel, Askeladden Capital Management LLC, Jeff Sands, Shawn Kravetz, Ryan Oviatt and Boyd Roberts (collectively the "Participants") filed a definitive proxy statement and accompanying proxy card with the SEC on May 20, 2025, as amended on May 21, 2025, to be used in soliciting proxies in connection with the 2025 annual meeting of shareholders (the "Annual Meeting") of AstroNova, Inc. (the "Company"). All shareholders of the Company are advised to read the Proxy Statement and other documents related to the solicitation of proxies, each in connection with the Annual Meeting, by the Participants, as they contain important information, including additional information related to the Participants, including a description of their direct or indirect interests by security holdings or otherwise. The Proxy Statement and an accompanying GOLD proxy card will be furnished to some or all of the Company's stockholders and is, along with other relevant documents, available at no charge on the SEC website at http://www.sec.gov, or by contacting Samir Patel at 1452 Hughes Road, Suite 200 #582, Grapevine, TX, 76051.

1 These topics are discussed in extensive detail in our 39-page "Primary Research Analysis" published on June 3, 2025. https://www.askeladdencapital.com/wp-content/uploads/2025/06/2025-06-03-Askeladden-Capital-Shares-Primary-Research-With-AstroNova-Shareholders.pdf

2 How a Hedge Fund Saved Olive Garden by Making its Breadsticks Better. Vanity Fair, April 2016. https://www.vanityfair.com/news/2016/04/olive-garden-breadsticks-starboard?srsltid=AfmBOorNb_srx0Lo3glugB1aWb6ZEyYEQD6ISm3uKyHjOR0dyFn9sSiL

3 ISS and Glass Lewis Recommend for All Twelve of Starboard's Nominees for Darden. September 30, 2014. https://www.prnewswire.com/news-releases/iss-and-glass-lewis-recommend-for-all-twelve-of-starboards-nominees-for-darden-277636341.html

4 Starboard's Jeff Smith resigns as Darden Chairman. Reuters. April 2016. https://www.reuters.com/article/us-darden-chairman-idUSKCN0X21FE/#:~:text=Starboard%20launched%20a%20public%20battle,its%20flagship%20Olive%20Garden%20chain

5 Mr. Woods' promise was made on the Q4 FY 2022 earnings conference call transcript on April 14, 2022; resolution of the issue is discussed in the FY2024 Form 10-K filed April 12, 2024. For more analysis, please refer to our 39-page "Primary Research Analysis" published on June 3, 2025. https://www.askeladdencapital.com/wp-content/uploads/2025/06/2025-06-03-Askeladden-Capital-Shares-Primary-Research-With-AstroNova-Shareholders.pdf

6 May 2023 Sidoti Micro-Cap Virtual Conference - Call Transcript.

7 The inventory days on hand metric is referenced on page 31 of AstroNova's Q1 FY26 Form-10Q, filed June 6, 2025. Data for prior years is sourced from the relevant Form 10-K.

8 AstroNova's Q4 FY24 earnings release from March 22, 2024 provided guidance for FY25 and FY26. The Q4 FY25 earnings release disclosed that EBITDA declined in FY25, and newly-provided FY26 guidance is below levels reported in FY24, and substantially below original guidance then provided for FY26.

9 MTEX Acquisition Announcement 8-K and MTEX Acquisition Call Transcript, May 9, 2024.

10 MTEX financial results are disclosed in the relevant Forms 10-Q for FY25 and FY26, with the goodwill impairment disclosed in the Form 10-K for FY25.

11 AstroNova Q2 FY25 Earnings Call Transcript, September 16, 2024. Refer to prior footnote as well.

12 AstroNova shareholder letter published June 13, 2025.

13 "Four steps to success for new CEOs." McKinsey. April 2023. https://www.mckinsey.com/featured-insights/future-of-asia/four-steps-to-success-for-new-ceos

14 AstroNova: Trojan Label Customer's Perspective. In Practise - Published May 31, 2025. https://inpractise.com/articles/astronova-trojan-label-customers-perspective

15 Please refer to AstroNova's proxy statements from FY20 - FY25.

16 Form 8-K Item 5.02, Compensatory Arrangements, filed June 16, 2025. Page 2.

17 No other texts or emails have since been sent or received between Askeladden and AstroNova's Board. We have redacted a shareholder's name to protect their privacy, and added surnames and roles in brackets for clarity, but it is otherwise verbatim.

18 These topics are discussed in extensive detail in our 39-page "Primary Research Analysis" published on June 3, 2025. https://www.askeladdencapital.com/wp-content/uploads/2025/06/2025-06-03-Askeladden-Capital-Shares-Primary-Research-With-AstroNova-Shareholders.pdf

19 May 2025 report by Objective Investment Banking & Valuation. https://www.objectiveibv.com/wp-content/uploads/2025/05/Objective-Aerospace-Defense-Industry-Report-Q1-2025-Final.pdf

20 2023 report by Institute for Mergers, Acquisitions, and Alliances. https://imaa-institute.org/blog/median-enterprise-value-to-ebitda-and-revenue-multiples/

21 "Warburg Pincus and Berkshire Partners' $3 bn Acquisition of Triumph Group." Merger Insight, March 7, 2025. https://www.mergersight.com/post/berkshire-hills-bancorp-and-brookline-bancorp-1-1-billion-merger-of-equals-1#:~:text=For%20the%20trailing%20twelve%20months,multiple%20of%20approximately%2016.6x.

22 Refer to AstroNova's Form 10-K for FY25 for segment reporting. AstroNova's Form 10-Q filed December 7, 2017, explains on page 8 that "The Honeywell Agreement also provides for minimum royalty payments of $15.0 million, to be paid over the next ten years." A more detailed explanation of royalty payments, payable through September 30, 2026, are discussed on pages 6, 7, and 8 of AstroNova's Form 8-K filed October 4, 2017 disclosing contractual terms of the Honeywell Asset Purchase and License Agreement.

SOURCE: Askeladden Capital Management LLC

View the original press release on ACCESS Newswire:

https://www.accessnewswire.com/newsroom/en/banking-and-financial-services/askeladden-town-hall-spotlights-clear-choice-for-astronova-hands-on-1040200