Crunchfish AB notes that it has received a positive International Preliminary Report on Patentability (IPRP) following its PCT demand examination for a privacy innovation related to its governed offline payments architecture supporting payment system resilience.

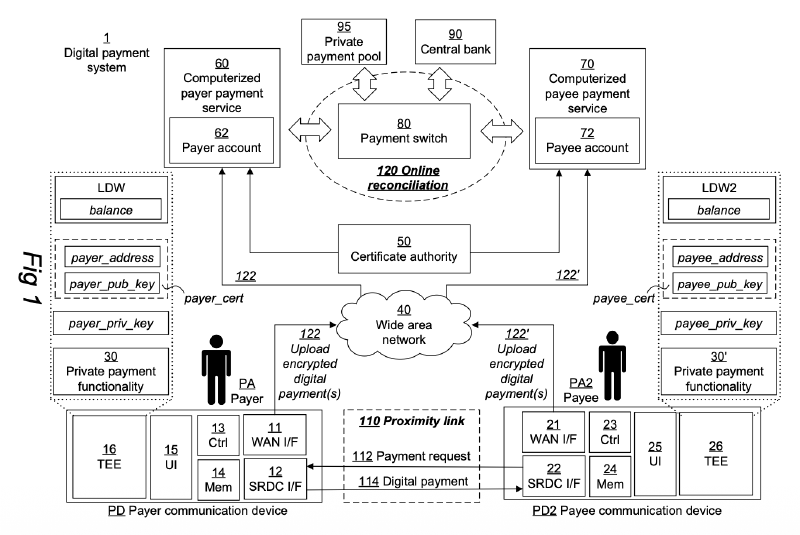

Figure 1: The privacy-preserving architecture of the governed offline model.

Privacy remains a core design consideration in digital money systems. Surveys conducted during the development of the digital euro consistently show privacy ranking as one of the most important features for the public, even ahead of resilience. At the same time, recent disruptions have highlighted the systemic risks that arise when digital payment systems or their backend functions become temporarily unavailable.

Why this innovation matters for central banks

For central banks and payment system operators, offline payments are increasingly recognised as an essential component of payment system resilience. Digital payments have become critical infrastructure in modern economies. When digital payment systems or their backend infrastructure becomes temporarily unavailable, whether due to outages, cyber incidents or broader disruptions, the ability for citizens and businesses to continue transacting becomes essential.

Crunchfish's governed offline architecture addresses this challenge by enabling digital payments to continue functioning even when the payment system itself is temporarily unavailable, while still maintaining regulatory oversight and financial system integrity. This creates a credible architectural path for offline functionality in CBDC systems, instant payment infrastructures and digital wallet ecosystems.

One of the long-standing challenges in designing digital currency systems has been balancing three objectives:

- resilience

- privacy

- regulatory compliance

The governed offline model demonstrates that these objectives can be reconciled through architectural design rather than policy trade-offs, an increasingly central topic in discussions on monetary and payment system architecture.

Offline architecture impact on privacy

Legacy approaches to offline digital payments, often referred to as immediate offline models, attempt to replicate cash by moving digital value directly onto devices. While such systems appear to promise cash-like anonymity, they typically require central reconciliation mechanisms to prevent double spending, fraud, money laundering and terrorist financing. Once reconciliation mechanisms are introduced, the perceived anonymity largely disappears because transactions must ultimately be reconciled and validated centrally.

Crunchfish's governed offline architecture takes a different approach. Instead of attempting to replicate physical cash digitally, the architecture ensures that offline transactions remain visible only to the remitting financial institution, such as the payer's bank or payment service provider, while avoiding the creation of new central repositories of transaction data. Governed offline payments operate as a layer-2 architecture above the existing payment systems.

Even when seamlessly integrated with existing payment applications, offline execution remains separated from the underlying payment infrastructure. This separation resembles the relationship between cash and bank deposits. When cash is withdrawn from an ATM, there is no technical mechanism linking the withdrawal of digital funds to how that cash is later spent. Governed offline uniquely maintains a similar separation through its layer-2 architecture. Cash achieves privacy through anonymity. Digital money must achieve privacy through architecture.

Within this architecture, the patent describes a mechanism where the payer's bank or payment service provider can pay by proxy on behalf of the payer. As a result, the payment remains visible only to the payer's chosen financial institution, while merchants, networks and other ecosystem participants do not gain access to the payer's identity. This architecture allows the same privacy model to be applied both online and offline, enabling users to mark payments as private or to have private payments enabled by default.

Another architectural property of governed offline is the absence of token chains, which are common in token-based immediate offline models. In such designs, chains of tokens must often be reconstructed during reconciliation to discover double spending, which can inadvertently reveal transaction relationships. This removes a key privacy weakness in many token-based CBDC architectures, making privacy a property of the monetary architecture itself.

Governed offline also makes it technically possible to support fully anonymous offline transactions, if permitted by policy and payment system governance. Such transactions can occur directly between offline wallets, where only debit and credit balance updates are recorded without revealing the identity of the payer or payee. Another possible approach is to allow the payer identity itself to remain anonymous, like a prepaid cash card without KYC requirements. This concept is covered in an adjacent Crunchfish patent application related to governed offline payments.

In practice, anonymity and privacy are likely to be governed by transaction thresholds defined by payment system policy. Smaller transactions may be allowed to remain anonymous, while larger transactions remain private but identifiable to the payer's financial institution. Because governed offline executes this logic within a trusted offline wallet, these rules can be enforced securely even when the payment system itself is temporarily unavailable.

Figure 2 - Privacy and anonymity thresholds in governed offline payments?

Figure 2: Privacy and anonymity in governed offline payments can be governed through policy-defined transaction thresholds, allowing system operators to balance financial privacy, regulatory oversight and payment system resilience.

CEO comment

"This is a strategically important patent application for Crunchfish as it uniquely balances resilience, privacy, and regulatory compliance. Digital money only works if people trust it. That trust depends on a resilient and privacy-preserving payment architecture. Governed offline addresses both by strengthening resilience while preserving privacy within the regulated financial system." - Joachim Samuelsson, CEO, Crunchfish

Research and analytical foundation

The privacy architecture described in the patent application builds on the analytical framework presented in Crunchfish's whitepaper: Offline Payments at Scale as Digital Money.

The paper introduces the BIG Analytical Framework, evaluating offline payment architectures across three dimensions:

- Bankable

- Implementable

- Governed

The framework analyses how different offline architectures behave when scaled to national payment systems, including how governed offline architectures can combine resilience, privacy and regulatory compatibility.

International patent application

The examination concerns Crunchfish's international patent application WO2025226204, describing a method for preserving user privacy in offline digital payments while maintaining compatibility with the regulatory and operational requirements of modern payment systems. The international patent examiner has concluded that the invention and its 33 claims meet the key patentability criteria of novelty and inventive step, allowing the application to proceed toward national patent phases.

The patent application has priority from April 2024, and Crunchfish expects to select jurisdictions for national filings before October 2026. If granted, the patent may remain valid until 2044. The application forms part of Crunchfish's broader intellectual property portfolio for governed offline payments, which currently includes 15 patent applications covering resilient offline digital payment architecture.

Attachments

The published PCT patent application WO2025226204 is attached to this press release.

For more information, please contact:

Joachim Samuelsson, CEO of Crunchfish AB

+46 708 46 47 88

joachim.samuelsson@crunchfish.com

This information is Crunchfish AB obliged to publish in accordance with the EU Market Abuse Regulation. The information was provided by the above for publication on March 16th, 2026, at 08:00 CET.

Västra Hamnen Corporate Finance AB is the Certified Adviser. Email: ca@vhcorp.se. Telephone +46 40 200 250.

About Crunchfish - crunchfish.com

Crunchfish is a deep fintech company developing patented governed offline payments technology for payment systems, banks, and payment applications. Its reservation-based Layer-2 architecture enables offline payments to operate as digital money, preserving central ledger authority, bounded exposure, and liquidity anchored within regulated institutions. By structurally aligning banking economics, scalable deployment, and governance continuity, Crunchfish enables offline capability at institutional scale without creating parallel forms of money or unmanaged credit risk. Crunchfish is listed on the Nasdaq First North Growth Market.