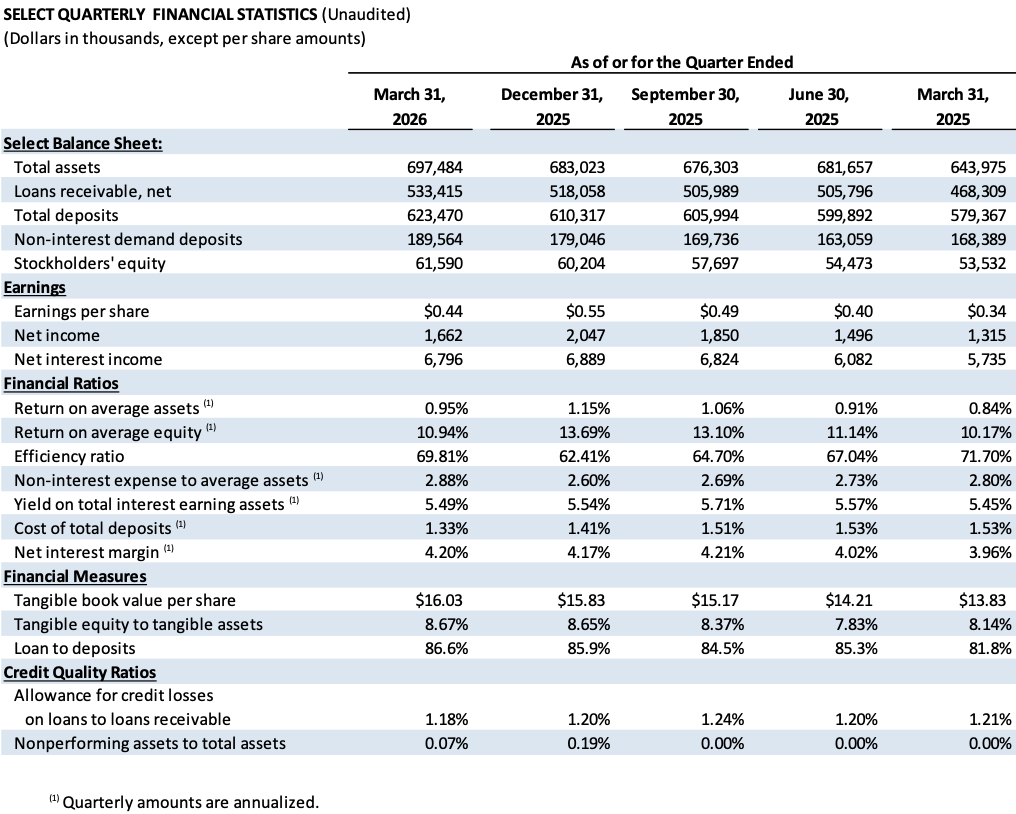

2026 First Quarter Financial Highlights:

Quarterly net income of $1.7 million, or $0.44 earnings per share.

Loans increased $15.4 million during the first quarter of 2026, or 11.9% annualized growth rate.

Deposits increased $13.2 million during the first quarter of 2026, or 8.7% annualized growth rate.

Net interest margin of 4.20% during the first quarter of 2026 compared to 4.17% during the fourth quarter of 2025.

Total cost of deposits of 1.33% during the first quarter of 2026 compared to 1.41% during the fourth quarter of 2025.

Capital ratios remained well above regulatory requirements.

TACOMA, WA / ACCESS Newswire / April 30, 2026 / Commencement Bancorp, Inc. (OTCQX:CBWA) (the "Company", "we," or "us"), the parent company of Commencement Bank (the "Bank"), reported net income of $1.7 million, or $0.44 per share, for the first quarter of 2026. Comparable earnings were $1.3 million, or $0.34 per share, for the first quarter of 2025 and $2.0 million, or $0.55 per share, for the fourth quarter of 2025. The Bank recorded return on average assets of 0.95% for the first quarter of 2026, compared to 0.84% for the first quarter of 2025 and 1.15% for the fourth quarter of 2025.

"We're happy to report nearly 30% increase in year-over-year earnings, driven by our exceptional bankers and the sustained momentum we've built quarter after quarter. This is what happens when great people, disciplined execution, and a clear vision come together. We're starting to hit our stride," said John E. Manolides, Chief Executive Officer.

"We're very pleased with our first quarter results - our best first quarter on record. Loan demand continues to be strong as evidenced by our double-digit growth stemming from our ongoing outbound calling efforts and heightened brand. We're poised to continue accelerating organic growth on both sides of the balance sheet. The recent announcement and addition of our new Healthcare Banking team is being well received, and their pipeline already reflects strong activity. We look forward to welcoming their client base and we're optimistic it will be a catalyst for sustainable growth in the quarters to come," stated Nigel L. English, President & Chief Operating Officer.

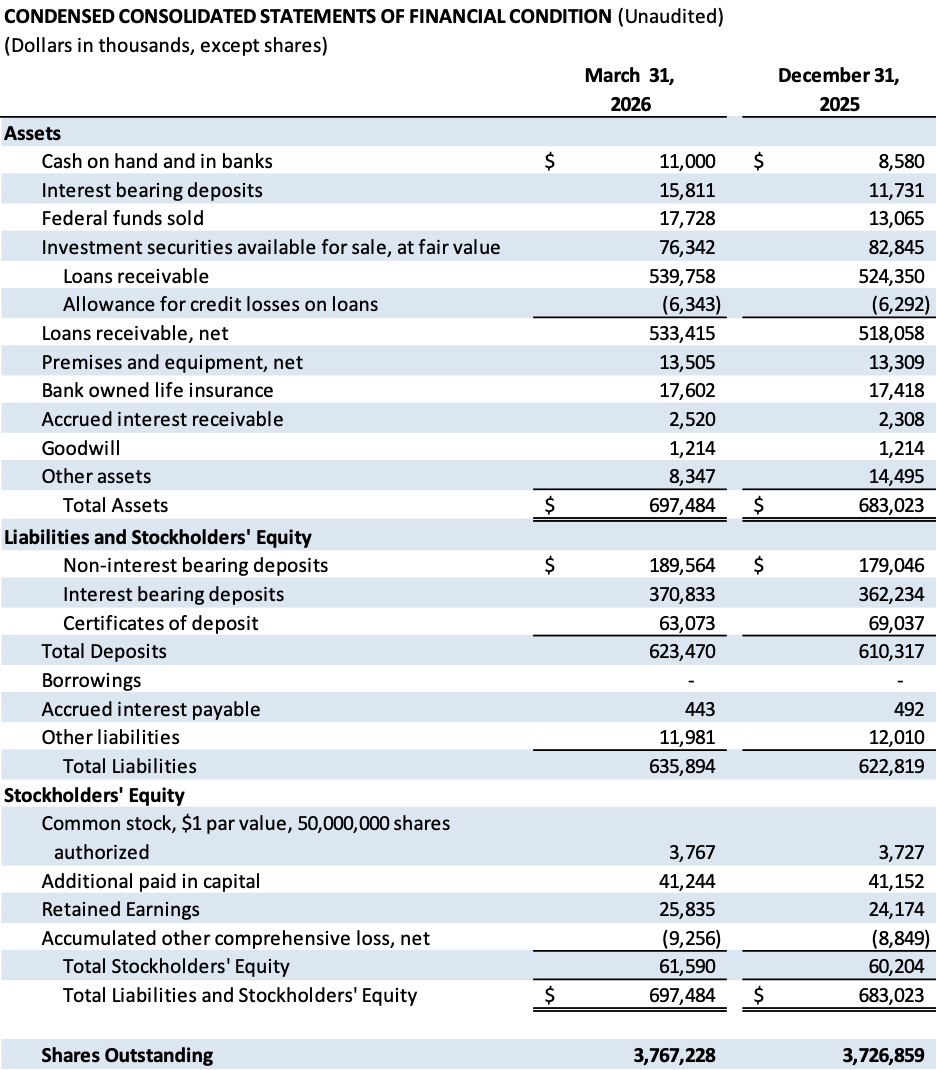

Balance Sheet

Total assets increased $14.5 million to $697.5 million at March 31, 2026 from $683.0 million at December 31, 2025.

Investment securities available for sale decreased $6.5 million, or 7.8%, to $76.3 million at March 31, 2026 from $82.8 million at December 31, 2025. This decrease was due to principal payments of $5.7 million, including the early redemption of one security with par balance of $3.5 million, and an increase in unrealized losses of $786,000.

Loans receivable increased $15.4 million, or 11.9% annualized, to $539.8 million at March 31, 2026 from $524.4 million at December 31, 2025, due to loan originations, offset by scheduled loan payments. The Bank originated commitments of $50.4 million during first quarter of 2026 compared to $38.7 million during the fourth quarter of 2025 and $20.8 million during the first quarter of 2025.

Total deposits increased $13.2 million, or 8.7% annualized, to $623.5 million at March 31, 2026 from $610.3 million at December 31, 2025. Noninterest bearing deposits, as a percentage of total deposits, increased to 30.4% at March 31, 2026, compared to 29.3% at December 31, 2025.

Credit Quality

The Bank had nonperforming assets of $488,000, or 0.07% of total assets, at March 31, 2026, compared to $1.3 million, or 0.19% of total assets, at December 31, 2025. The decrease was related to the resolution of one relationship and the charge-off of another relationship to its net realizable value. The Bank recorded charge-offs of $125,000 during the first quarter of 2026. The allowance for credit losses to loans receivable remains strong at 1.18% at March 31, 2026, compared to 1.20% at December 31, 2025.

The percentage of classified loans (loans rated Substandard or worse) to loans receivable decreased to 0.90% at March 31, 2026, from 2.06% at December 31, 2025, due primarily to the full payoff of one credit of $5.2 million. The Bank proactively downgrades loans if the borrower is experiencing financial difficulties and upgrades loans if the borrower demonstrates sustained financial performance.

Liquidity

The Bank has ample liquidity with both on-and off-balance sheet sources. Total on-balance sheet liquidity of $120.9 million, or 17.3% of total assets, at March 31, 2026, includes unencumbered cash, cash equivalents and investment securities. The Bank also had access to available Federal Home Loan Bank advances, Federal Reserve's discount window, and federal funds lines with correspondent banks of $215.0 million at March 31, 2026.

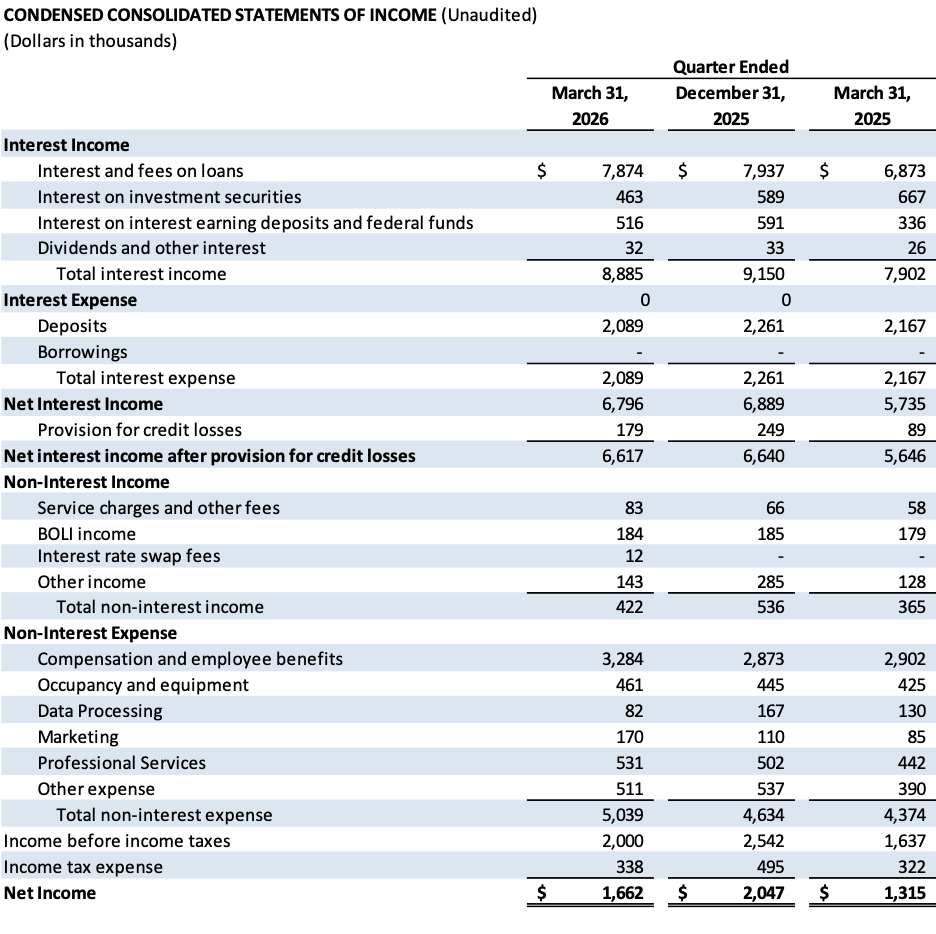

Income Statement

Net interest income increased $1.1 million, or 18.5%, compared to the first quarter of 2025 due to the increase in interest income of $983,000 and a decrease in interest expense of $78,000. Interest income increased from the increase of average interest earning assets of $68.7 million during the first quarter of 2026 compared to the first quarter of 2025. Net interest income was impacted by the reduction of the federal funds rate of 75 basis points ("bps") in the latter half of 2025, reducing variable rate loans and new loan origination pricing. During the first quarter of 2026, the Company had average variable loans of $103.4 million. Net interest income decreased $93,000, or 1.35%, during the first quarter of 2026 compared to the fourth quarter of 2025 due to the decrease in interest income of $265,000, offset by the decrease in interest expense of $172,000. These decreases were the result of the previously mentioned federal funds rate cuts and also fewer days in the first quarter compared to fourth quarter.

Net interest margin ("NIM") increased 24 bps to 4.20% during first quarter of 2026 from 3.96% during the first quarter of 2025 due to a combination of an increase in loan yields of 17 bps and a reduction of total deposit costs of 20 bps, offset by compression due to the reduction of federal funds rates. NIM increased 3 bps compared to 4.17% during the fourth quarter of 2025 primarily due to the decrease in deposit costs of 8 bps, partially offset by reduction in yield on investment securities of 7 bps.

Interest income on loans increased $1.0 million, or 14.6%, during the first quarter of 2026 compared to the first quarter of 2025 due primarily to an increase in average balances of $53.2 million. Interest income on loans decreased $63,000 during the first quarter of 2026 compared to the fourth quarter of 2025 due primarily to fewer days in the first quarter. The yield on net loans decreased 2 bps to 6.16% for the first quarter of 2026 from 6.18% for the fourth quarter of 2025 due to the previously mentioned variable loan repricing, offset partially by higher yields on new loan originations and renewals, and higher repricing rates on the adjustable portfolio.

Interest income on investments decreased $204,000 during the first quarter of 2026 compared to the first quarter of 2025 due to a decrease in average balances of $10.4 million due primarily to principal payments. Interest income on investments decreased $126,000 during the first quarter of 2026 compared to the fourth quarter of 2025 due primarily to the early redemption of a security with significantly higher yield in addition to the negative interest impacts of the $40.0 million interest rate swap given the lower rate environment.

Interest income on interest earning deposits and federal funds sold increased $180,000 during the first quarter of 2026 compared to the first quarter of 2025 due to an increase of the average balances of $25.8 million, offset slightly by the decrease in market rates. Interest income on interest earning deposits and federal funds sold decreased $75,000 during the first quarter of 2026 compared to the fourth quarter of 2025 due to the reduction in short term rates and a reduction of the average balances of $2.6 million.

Interest expense on deposits decreased $78,000, or 3.6%, during the first quarter of 2026 compared to the first quarter of 2025 due to a decrease in exception pricing rates, offset by an increase in the average balance of interest-bearing deposits of $41.9 million. Total cost of deposits decreased 20 bps to 1.33% for first quarter of 2026 compared to 1.53% for the first quarter of 2025. Interest expense on deposits decreased $172,000 during the first quarter of 2026 compared to the fourth quarter of 2025 due to a decrease in exception pricing rates, offset by an increase in the average balance of interest-bearing deposits of $2.8 million. Total cost of deposits decreased 8 bps compared to 1.41% for the fourth quarter of 2025. Noninterest bearing demand deposits represent 30.4% of total deposits at March 31, 2026 compared to 29.3% at December 31, 2025.

Total non-interest income increased $57,000, or 15.6%, during the first quarter of 2026 compared to the first quarter of 2025 due to an increase in service charges from the increase in customer relationships. Total non-interest income decreased $114,000 during the first quarter of 2026 compared to the fourth quarter of 2025 due primarily to the decrease in fees recognized from nonreciprocal deposit sales based on lower average balances sold during first quarter of 2026.

Total non-interest expense increased $665,000 during the first quarter of 2026 compared to the first quarter of 2025 due to an increase in total compensation. Total non-interest expense increased $405,000 during the first quarter of 2026 compared to the fourth quarter of 2025 due primarily to an increase in compensation and employee benefits related to employee merit increases, additional stock compensation expense from newly granted awards, and an increase in payroll taxes as certain thresholds have not yet been met for the year.

Income tax expense increased $16,000 during the first quarter of 2026 compared to the first quarter of 2025 due primarily to an increase in net income, offset substantially by an increase in tax-exempt loans. The effective tax rate for the first quarter of 2026 was 16.9% compared to 19.7% during the first quarter of 2025. Income tax expense decreased $157,000 during the first quarter of 2026 compared to the fourth quarter of 2025 due primarily to an increase in tax-exempt loans.

###

About Commencement Bancorp, Inc.

Commencement Bancorp, Inc. is the holding company for Commencement Bank, headquartered in Tacoma, Washington. Commencement Bank was formed in 2006 to provide traditional, reliable, and sustainable banking in Pierce, King, Kitsap, and Thurston counties and the surrounding areas. Their team of experienced banking experts focuses on personal attention, flexible service, and building strong relationships with customers through state-of-the-art technology as well as traditional delivery systems. As a local bank, Commencement Bank is deeply committed to the community. For more information, please visit www.commencementbank.com. For information related to the trading of CBWA, please visit www.otcmarkets.com.

For further discussion, please contact the following:

John E. Manolides, Chief Executive Officer | 253-284-1802

Nigel L. English, President & Chief Operating Officer | 253-284-1801

Brandi Parker, Executive Vice President & Chief Financial Officer | 253-284-1803

Forward-Looking Statement Safe Harbor: This news release contains comments or information that constitutes forward-looking statements (within the meaning of the Private Securities Litigation Reform Act of 1995) that are based on current expectations that involve a number of risks and uncertainties. Forward-looking statements describe Commencement Bancorp, Inc.'s projections, estimates, plans and expectations of future results and can be identified by words such as "believe," "intend," "estimate," "likely," "anticipate," "expect," "looking forward," and other similar expressions. They are not guarantees of future performance. Actual results may differ materially from the results expressed in these forward-looking statements, which because of their forward-looking nature, are difficult to predict. Investors should not place undue reliance on any forward-looking statement, and should consider factors that might cause differences including but not limited to the degree of competition by traditional and nontraditional competitors, declines in real estate markets, an increase in unemployment or sustained high levels of unemployment; changes in interest rates; greater than expected costs to integrate acquisitions, adverse changes in local, national and international economies; changes in the Federal Reserve's actions that affect monetary and fiscal policies; changes in legislative or regulatory actions or reform, including without limitation, the Dodd-Frank Wall Street Reform and Consumer Protection Act; demand for products and services; changes to the quality of the loan portfolio and our ability to succeed in our problem-asset resolution efforts; the impact of technological advances; changes in tax laws; and other risk factors. Commencement Bancorp, Inc. undertakes no obligation to publicly update or clarify any forward-looking statement to reflect the impact of events or circumstances that may arise after the date of this release.

SOURCE: Commencement Bank

View the original press release on ACCESS Newswire:

https://www.accessnewswire.com/newsroom/en/banking-and-financial-services/commencement-bancorp-inc.-announces-first-quarter-2026-results-1162901