Q1 2026

(Q4 2025)

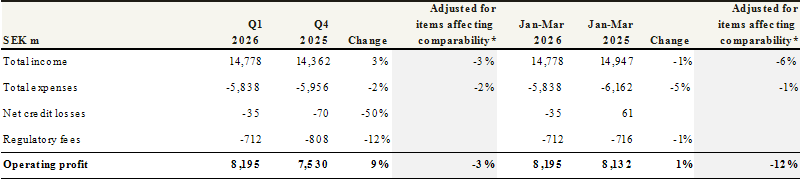

- Operating profit climbed by 4% to SEK 8,195m (7,530)

- VAT refund of SEK 1,127m (196)

- Return on equity increased to 13.6% (13.0)

- Earnings per share grew to SEK 3.21 (3.01)

- The C/I ratio improved to 39.5% (41.5)

- The credit loss ratio was 0.01% (0.01)

- The common equity tier 1 ratio was 17.2% (17.6)

January - march 2026

(January - march 2025)

- Operating profit climbed to SEK 8,195m (8,132)

- VAT refund of SEK 1,127m (-)

- Return on equity increased to 13.6% (12.9)

- Earnings per share grew to SEK 3.21 (3.19)

- The C/I ratio was 39.5% (41.2)

- The credit loss ratio was 0.01% (-0.01)

- The common equity tier 1 ratio was 17.2% (18.4)

Stable net interest income and growing savings business growth

Net interest income was stable compared to the previous quarter, in spite of negative day and foreign exchange effects, as well as lagging effects on interest margins from lower market rates. In the UK and the Netherlands, the trend of increasing household and corporate lending continued. The Bank's market share in these countries is small, and there is significant long-term growth potential. In Sweden and Norway, demand for loans was more subdued during the quarter, in line with muted macroeconomic developments. In both Sweden and Norway, the net inflow into the Bank's funds remained strong, with a market share that far exceeded the market share of outstanding volume.

Lower expenses and good credit quality

The greater focus on efficiency in recent years has reduced the running cost base at the Bank, offsetting both general inflation and the annual salary adjustments that come into effect at the start of every year. Compared with the previous quarter, expenses went down by 2%, while compared with the corresponding quarter during the previous year, expenses were down by 1% after adjustments for items affecting comparability. Credit quality remained strong with a credit loss ratio of 0.01%.

A position of financial strength

The Bank distinguishes itself as one of the world's most stable banks, which is reflected in the fact that no other privately owned bank in the world has a higher overall credit rating from the leading rating agencies. This is achieved through a locally connected, long-term, and customer-centric business model with low risk tolerance and a strong financial position. After anticipated dividends during the quarter amounting to SEK 2.93 per share, corresponding to 91% of profit for the quarter, the common equity tier 1 ratio was 2.50 percentage points above the regulatory requirement by the Swedish Financial Supervisory Authority. This level was thus within the Bank's target range of 1-3 percentage points above the regulatory requirement. The Bank's financial strength creates trust and confidence, as well as prerequisite for continued stable and profitable growth.

* Items affecting comparability consist of foreign exchange effects, non-recurring items and special items, which are presented in the tables on pages 5 and 6.

Information regarding the press conference

A press conference will be held on 22 April 2026 at 08:30 a.m. (CET).

Press releases, presentations, a fact book and a recording of the press conference will be available at handelsbanken.com/ir.

The interim report for January - June 2026 will be published on 15 July 2026.

For further information, please contact:

Michael Green, President and Chief Executive Officer

Tel: +46 (0)8 22 92 20

Mårten Bjurman, CFO

Tel: +46 (0)8 22 92 20

Peter Grabe, Head of Investor Relations

Tel: +46 (0)70 559 11 67, peter.grabe@handelsbanken.se

This information is of the type that Svenska Handelsbanken AB is obliged to make public pursuant to the EU Market Abuse Regulation and the Swedish Securities Markets Act. The information was submitted for publication through the agency of the contact person set out above, at 07:00 a.m. CET on 22 April 2026.

For more information about Handelsbanken, please go to: handelsbanken.com